Rental Moratorium Ends, Rental Yield Holds Stable

The Australian rental market came under scrutiny in March 2020, when COVID-19 first hit and job losses were anticipated. Fears of not being able to meet rental payment obligations were voiced, as well as fears of mortgage payment arrears. All levels of Governments deployed a range of policies, including a rental eviction moratorium, to ensure renters impacted by COVID-19 are able to maintain their residency. Other key measures were introduced to provide equal protection to landlords.

Rental Yields

Rental yields are one of the key indicators relied upon when investors evaluate the health of the rental market. Many predicted a fall in rental yield, due to an expected fall in rental prices. While this may be true in some cases, particularly in heavily COVID-19 impacted capital cities and suburbs, rental yields have, as an overall, remained resilient.

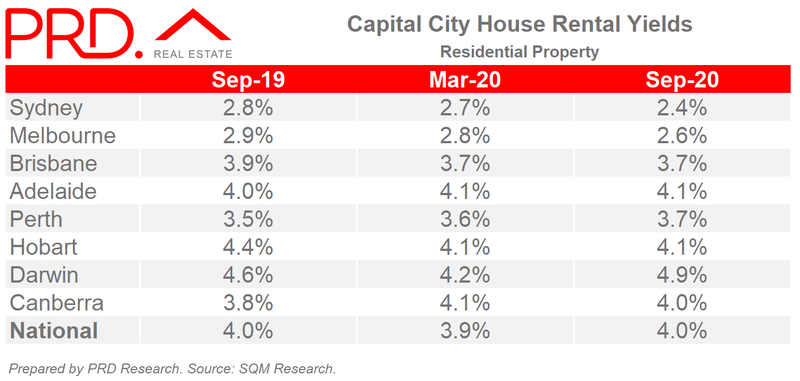

The national rental yield for all houses in September 2019 sat at 4.0%, which dipped ever so slightly to 3.9% in March 2020, and is now back at 4.0% in September 2020.

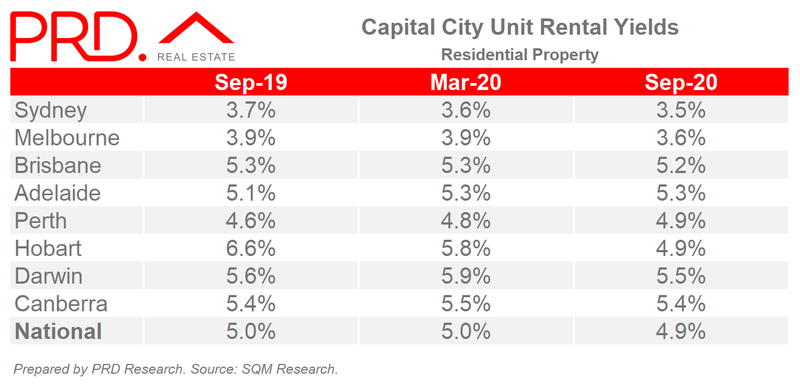

Similarly, the national rental yield for all units sat at 5.0% in September 2019, remained at 5.0% in March 2020, and dipped slightly to sit at 4.9% in September 2020.

Rental Eviction Moratorium

September sees the National Cabinet’s (Federal Government) rental eviction moratorium conclude. Understandably this has caused high uncertainty in the market, both for renters and landlords. The majority of States and Territories have extended the rental eviction moratorium anywhere from December 2020 to April 2021, with various support packages below. A quick summary for each is provided below:

- Queensland: Rental eviction moratorium is extended until 31st December 2020 on a financial hardship basis. This announcement has been supported by the Real Estate Institute of Australia as a sensible and multi-stakeholder approach.

- New South Wales: Current residential and tenancy support grants/policies have been extended an extra six months, to March 2021.

- Australian Capital Territory: Rental eviction moratorium extended until January 2021.

- Tasmania: Rental eviction moratorium extended until December 2020.

- Victoria: Rental eviction moratorium extended until April 2021, with a varying range of support measures in place for tenants and homeowners.

- South Australia: An extension of the tenant support program has been made until 28th March 2021, or until the end of the South Australian emergency provisions.

- Northern Territory: At the time of writing, an announcement is still pending.

- Western Australia: Rental eviction moratorium extended until March 2021, with hotline support in place for owners and tenants.

Moving Forward

A key reason as to why the national house and unit rental yields have remained stable amidst COVID-19 in the past 12 months to September 2020 is a combination of three forces in tandem: JobKeeper payments, mortgage holiday freezes, and rental eviction moratoriums.

The end or extension of the rental eviction moratorium has once again, as per when residential rental laws were re-negotiated in March 2020, caused uncertainties and imbalances in the market. This is particularly evident in light of mortgage holiday freezes ending (and not being extended) and JobKeeper payments being reduced on a two-tiered basis until March 2021.

Renters who have been, or are still, significantly impacted by COVID-19 benefit. They will be able to maintain their current residency and breathe a sigh of relief. Those who negotiated a rent reduction will see a benefit, as it assists with the household’s income flow. Landlords, on the other hand, are now faced with potentially higher mortgage payments; particularly those who froze their mortgages and have compounded interest, with potentially less rental income.

With the varying extension dates of rental eviction moratoriums (between December 2020 and April 2021) landlords may face the challenge of an end lease period, and the intricacies of either renewing (with the same tenant) or establishing a new agreement (with a new tenant).

The rental market has proven its resilience to date, continuously attracting investors and replenishing rental supply. It will be interesting to monitor the rental market in the next three to six months, and how current policy imbalances impact both renters and landlords.