Affordable & Liveable Property Guide 2nd Half 2019 - Sydney

A key finding in this report was that in order to identify affordable and liveable areas, suburbs with declining annual median house or unit price growth had to be considered. This was the same methodology applied in the 1st Half 2019¥ report. Therefore, instead of showcasing only suburbs with price growth (which was the trend in 2nd Half 2018µ report), it continued to be an exercise in minimising the decline in capital growth. This is good news for first home buyers because chosen affordable and liveable suburbs are now even more affordable.

Affordable Suburbs

A key finding in this report was that in order to identify affordable and liveable areas, suburbs with declining annual median house or unit price growth had to be considered. This was the same methodology applied in the 1st Half 2019¥ report. Therefore, instead of showcasing only suburbs with price growth (which was the trend in 2nd Half 2018µ report), it continued to be an exercise in minimising the decline in capital growth. This is good news for first home buyers because chosen affordable and liveable suburbs are now even more affordable.

Median property prices in Sydney softened by -8.6% for houses to $1,223,000 and by -6.4% for units to $474,750 from 2018 to 20191. Sale transactions declined over the same period, by

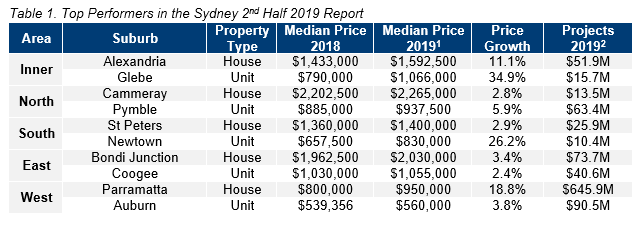

-26.0% for houses and -24.7% for units, which is reflective of the slower market conditions. By comparison, from 2017 to 2018 the median house price in Sydney dropped by -4.5%, and the median unit price dropped by -2.6%, while sale transactions fell -16.6% for houses and -26.6% for units. Thus, there has been more price cooling and reduction in market activity. Table 1 highlights top suburbs in Sydney based on price growth and total estimated value of projects commencing in the 2nd half of 20192.

In the 12 months to Q2 2019 the proportion of income to meet home loan repayments decreased by -2.6% in New South Wales (NSW)3. Despite this, the number of first home buyers entering into the market softened by -5.9%, indicating first home buyer confidence is still recovering. New Federal Government incentives and the latest Reserve Bank of Australia’s cash rate cuts should lift first home buyer confidence for the rest of 2019 and into 2020.

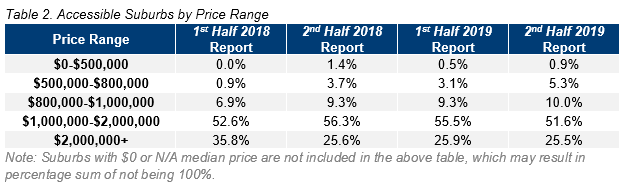

Table 2 provides the percentage of suburbs in Sydney that are available for house buyers.

Liveable Suburbs

The Sydney market has continued to move towards a more affordable property market. The price bracket of less than $500,000 continued to grow from the 1st Half 2019¥ report, from 0.5% to 0.9% in this report. This is admittedly lower than the quoted 1.4% in the 2nd Half 2018µ report, however it is possible that this was due to stock availability. First home buyers further rejoice as the $500,000-$800,000 price bracket continues to expand, from 9.3% in the 1st Half 2019¥ report to 10.0% in this report.

That said, the dominant price point in Sydney remains within the $1.0-$2.0M price bracket, accounting for 51.6% of sales transactions in the 2nd half of 2019. Although this is the lowest level seen in recent years, it represents a resilient middle of the range market. This is good news for current owner occupiers and investors, as they can be confident of sustainable capital growth.

Highly affordable suburbs (those with a maximum property sale price of the state average home loan3, plus a 165% deposit as per the 1st Half 2019¥ report), do exist. In this report, 119 suburbs are within this price range, an improvement compared with the 75 suburbs previously identified in the 1st Half 2019¥ report.

There is a unique phenomenon happening in the current Sydney market. A cooling in property prices has resulted in a higher number of affordable suburbs. However, this also means there were many suburbs with negative price growth (some at double digit negative price growth), and many suburbs failing to meet either the investment and/or liveability criteria.

In line with the methodology suburbs with price growth as close as possible to neutral (i.e. zero) were chosen, and to meet other criteria a premium of 150% for houses and 32% for units was added to the NSW average home loan. This is below the 1st Half 2019¥ report premium and below the level required to reach Sydney’s median house price and median unit price, indicating the recent market cooling has resulted in improved access to liveable suburbs in Sydney.

Considering all methodology criteria (property trends, investment, affordability, development, and liveability), Tables 3 and 4 identify key suburbs that property watchers should be on the lookout for.

Affordable & Liveable Suburbs

During Q2 2019, the Sydney rental market recorded a median rental price of $500 per week for houses4 and $540 per week for units4, representing stability in house rental market growth and a minor softening in the unit median rental price of -1.8%. These stable rent levels were achieved despite a 3.5% vacancy rate, which represented an increase in the 12 months to Q2 2019. Average yields of 2.9% (houses) and 3.8% (units) represent a slight upward trend in the 12 months to Q2 2019, which is reflective of the cooling movement in Sydney Metro area median property prices. Overall there are positive indicators within the Sydney Metro rental market, providing investors with confidence.

The 2nd half of 2019 is set for approximately $16.8B2 of development with a well-balanced focus on mixed-use, residential, and commercial projects, as well as significant spending on infrastructure and some industrial activity also. Key projects for the period include the $208.1M George Street Commercial Building and the $362.0M Richmond Road & Grange Ave Mixed Development, which will add 1,050 apartments to the Sydney market. Further, the $102.8M Marsden Park Residential Precinct will add an additional 775 units. Together, these projects highlight the strength of Sydney’s development pipeline for the 2nd half of 2019.

Methodology

This report analyses all suburbs in the Greater Sydney area, within a 20km radius of the Sydney CBD. The following criteria were considered:

- Property trends criteria – all suburbs have a minimum of 10 transactions for statistical reliability purposes. Based on market conditions, suburbs have either positive, or as close as possible to neutral price growth, between 2018 to 20191.

- Investment criteria – as of June 2019, all suburbs considered will have an on-par or higher rental yield than Sydney Metro, and an on-par or lower vacancy rate.

- Affordability criteria – identified suburbs have a median price below a set threshold. This was determined by adding percentage premiums to the NSW average home loan, which was $481,1693 as of Q2 2019. Premiums of 150% for houses and 32% for units were added, which were below those required to reach Sydney Metro’s median prices (154% for houses and 55% for units). This places the suburbs below Sydney’s median prices, meaning that the suburbs identified within this report are more affordable for buyers.

- Development criteria – all suburbs identified within this report have a high total estimated value of future development for the 2nd half of 20192, as well as a higher proportion of commercial and infrastructure projects. This ensures suburbs chosen show signs of sustainable economic growth, which in turn has a positive effect on the property market.

- Liveability criteria – this included ensuring all suburbs assessed have low crime rates, availability of amenities within a 5km radius (i.e. schools, green spaces, public transport, shopping centres and health care facilities), and an unemployment rate on-par or lower in comparison to the state average (as determined by the Department of Jobs and Small Business, March Quarter 2019 release).