2023: A three-speed economy and real-estate market?

From the Desk of the Chief Economist

The Reserve Bank of Australia (RBA) increased the cash rate for the 8th consecutive time in December 2022, which sees Australia closing the year with a 3.10% cash rate. In its publicly available documents, the RBA has continued its message of potential further cash rate increases in the near future, to pull down inflation back to the healthy 2-3.0% band.

Many Australians are facing pressure through being in a “mortgage cliff” situation, with their fixed-home loan rates due to expire in the next 3-6 months. What’s more, many in this category have not experienced a cash rate increase, and although have been rate-tested by their lender, have not budgeted for such a high mortgage re-payment increase.

With every aspect of life now more expensive, what can we expect in 2023? From a general economic perspective and specifically real estate? Those who can, those who are holding on, and those who cannot. Could a 3-speed economy and real-estate market emerge?

November Statement of Monetary Policy

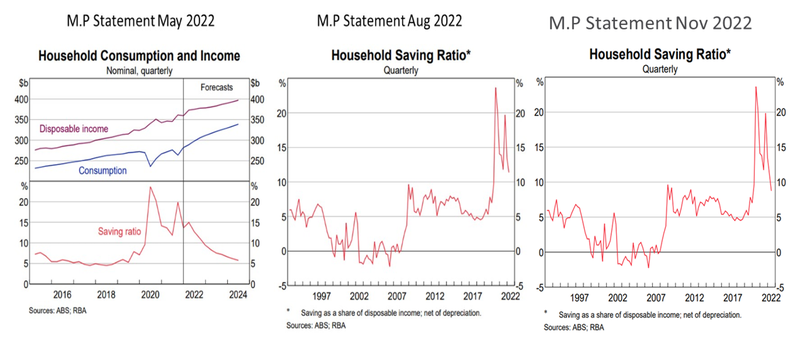

The RBA’s November statement of monetary policy indicated that Australia’s household savings ratio has declined rapidly, from more than 20.0% during COVID-19 to just under 10.0%. This suggests Australians are dipping into their reserves to adjust to inflationary pressures on living, to ensure that they are still able to afford their lifestyle.

The latest data from the Australian Bureau of Statistics (ABS) released Wednesday 7th December recorded household savings were at 6.9% in the September quarter of 2022. This is effectively a third of what Australians had in the September quarter of 2021, at 19.8%.

What is concerning is the speed at which household savings is declining. The RBA predicted the household saving ratio to return to a pre-COVID-19 “normal economy” level of approx. 5.0%. That said with the cost of living not predicted to come down anytime soon, and without a “thick buffer”, how long can the Australian household remain in a positive savings ratio?

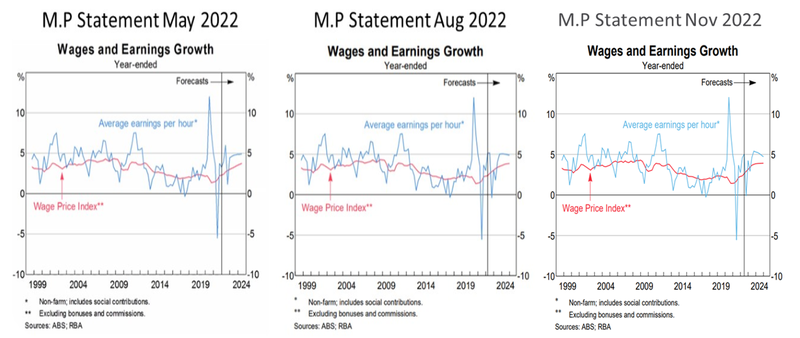

Interestingly, wages and earning growth have not changed between May, August, and November 2022 Statement of Monetary Policy.

Australians have experienced the highest wage growth in the past decade, regardless of employment type. Yet once wages grew, it seems to have stagnated, set to plateau in early 2024 at 4.8%. Meanwhile, headline inflation continues on an inclining path, creating a bigger gap between the ability to afford and save versus cost and spending.

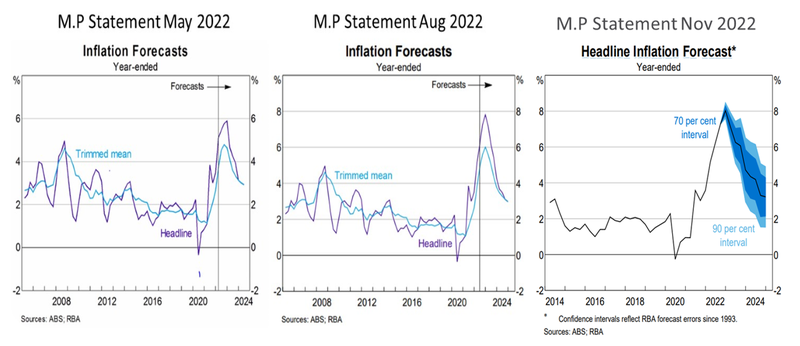

Headline Inflation predictions were revised in RBA’s November statement of monetary policy, to a higher peak of 8.1%. This is higher than May and August predictions. Month-by-month inflation data from the ABS did show a slight decline, to 6.9% for October 2022. That said the month-by-month data does not include key items such as gas and electricity.

Even so, the imbalance between wages and inflation will continue to grow. Put simply, we have an extra $50 in our pocket however living costs an extra $100. Further, the RBA’s target rate of approx. 3.0% by 2024 has not changed. This suggests further use of the cash rate as an ongoing tool to curb inflation, thus higher mortgage repayments in the future. All in all, this relates to households' savings declining further.

Will we have a three speed economy?

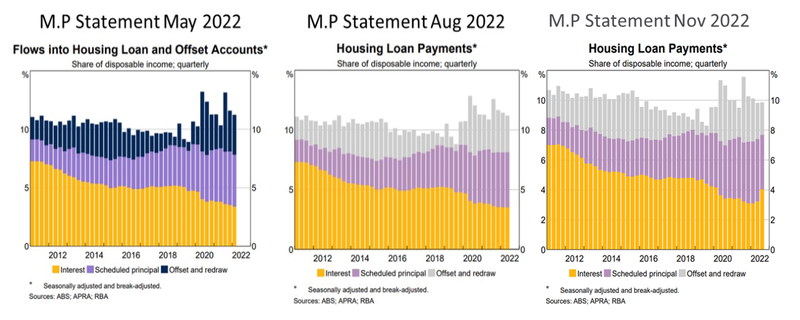

It is key to remember that many of the RBA’s graphs and predictions are aggregate, due to its charter and the lever/tools it can utilise. The RBA does provide disaggregated information, to ensure that it has full visibility of the underlying issues. However, as a whole, much of the communicated information is aggregate in nature.

A good example is the “Housing Loan Payments” graph, which shows the proportion change between interest paid, scheduled principal payments, and mortgage offset.

In this graph, mortgage offset payments have increased significantly during COVID-19, as many Australians took advantage of stable extremely low cash rate and higher disposable income. The “housing loan payments” graph have only moved marginally since the cash rate hikes, however, it has not fully captured all eight (to date).

When asked whether or not there is data to show a first home buyer’s ability to absorb the cash rate increase, especially those who bought in late 2020 onwards (pre-cash rate hike); the answer is unfortunately vague.

The RBA did communicate it is likely many first-home buyers (FHB) may face increased mortgage stress due to cash rate increases, even if they were tested against a higher rate. This means that an FHB may not be able to absorb cash rate increases unless the home is transitioned into an investment property, where they can shift additional costs to a tenant.

Therefore as an aggregate, the picture looks strong. However drilled down, not always. The same can be said for Household Savings. Overall, we are seeing a declining pattern, back to a “standard normal economy” savings rate of approximately 5.0%. Yet anecdotal data suggest separate demographics are already without savings or choosing between key items. Already the latest ABS data show a deep dip in discretionary spending, suggesting Australians are making calculated choices between essential and non-essential items.

This begs the question. Until there is stability in our cost of living and cash rate, will we see a three-speed economy? those who can, those who are holding on, and those who can not?

Moving forward – what can we expect for 2023?

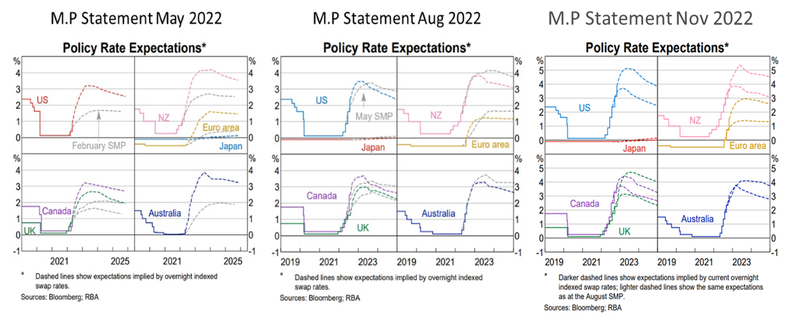

Policy rates expectations in RBA’s November statement of monetary policy have changed – for Australia and the rest of the world. Overall, policy rates are expected to peak at a higher point of 4.0% and stabilising at under 3.0%. This is a change from the August statement of monetary policy, with an expected peak of around 3.5%.

Technically speaking, a higher cash rate, if adopted by banks means higher interest, which will increase the cost of living pressures for owner-occupiers. If cash rates keep hiking, defaults in mortgages can be expected at best and recession at worst.

Should we worry? Yes and no. Mild recession is active in most major economies including China and the USA, which is starting to cause downward pressure on inflation.

A hope in 2023 is that we start to see inflation stabilise, largely due to lower property prices and aggregate demand. With this, a cash rate stabilisation is probable. But, clarity on when this will occur is uncertain. In aggregate, our household and business balance sheets are in strong shape. Separated accordingly, we may see a 3-speed economy taking shape. And with this, a multiplier effect on all industries, including the real estate market.