Increasing access to home ownership: the Catch-22

From the Desk of the Chief Economist - "Increasing access to home ownership: the Catch-22"

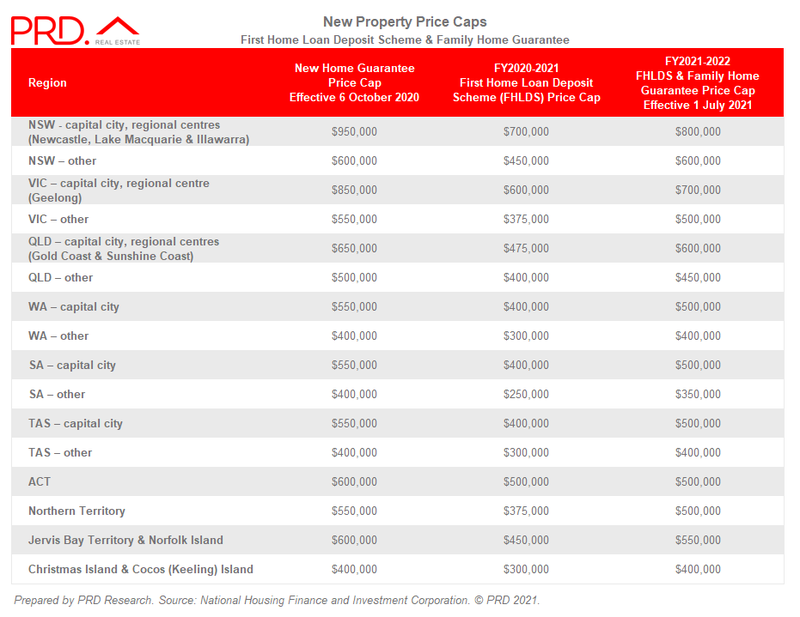

On 19th June 2021, the Australian Government announced new property price caps for the First Home Loan Deposit Scheme (FHLDS) and the Family Home Guarantee (FHG), which will apply from 1st July 2021.

These new price caps acknowledge that property prices have reached new heights across Australia and is part of the Government’s commitment to ensure Australians can continue to purchase a home as well as accommodate larger families.

Domain’s First Home Buyers Report 2021 cited that in most capital cities it takes a couple between 2 and 9 months longer to save a 20% house deposit of the average property price. Both the Real Estate Institute of Australia and the Government acknowledge that saving a deposit is the hardest part of getting into home ownership, thus both schemes will assist home buyers in achieving this, whilst the new price caps provide a more realistic landscape.

Increasing access to home ownership: Catch 22

The First Home Loan Deposit Scheme (FHLDS) allows first home buyers to purchase a home with only a 5% deposit without paying Lender’s Mortgage Insurance. 10,000 FHLDS places will be available to eligible first home buyers for the 2021-22 financial year.

Situation 1 – First home buyer in Brisbane, purchasing a second-hand home

· Maximum price: $600,000

· 5% deposit: $30,000

· First home owner grant: $0 (as it is second hand)

· Mortgage debt (other fees excluded): $570,000

Situation 2 – First home buyer in Melbourne, purchasing a new build property

· Maximum price: $850,000

· 5% deposit: $42,500

· First home owner grant: $0 (ineligible for a grant as property price is above $750,000)

· Mortgage debt (other fees excluded): $807,500

The Family Home Guarantee allows single parents to purchase a home with a 2% deposit, much in the same way as the FHLDS works. 10,000 places will be made available over 4 financial years from 1st July 2021, subject to the passage of legislation.

Situation 3 – Single parent in Lake Macquarie, not a first home buyer

· Maximum price: $800,000

· 2% deposit: $16,000

· First home owner grant: $0

· Mortgage debt (other fees excluded): $784,000

Situation 4 – Single parent in Gold Coast, also a first home buyer and buying a new build

· Maximum price: $600,000

· 2% deposit: $12,000

· First home owner grant: $15,000

· Mortgage debt (other fees excluded): $573,000

The New Home Guarantee has been extended with an additional 10,000 places available from 1st July 2021 – 30th June 2022 for eligible first home buyers purchasing a new home. It will now have a construction commencement timeframe of 12 months.

Situation 5 – First home buyer in Brisbane

· Maximum price: $650,000

· 5% deposit (if eligible for FHLDS also): $32,500

· First home owner grant: $15,000

· Mortgage debt (other fees excluded): $602,500

Moving forward

The Federal Budget 2021 emphasised access to home ownership for Australians.

This is due to the imbalance between property price growth and weekly family median income growth across Australia, and in particular the difficulty of saving a deposit for first home buyers and certain demographics.

The schemes introduced by the Government provide higher hope for those wanting to enter the property market. This is commendable, especially as the past 2-3 Federal Budgets did not address first home buyers directly.

However, looking at the mortgage debt figures which do not include any other fees (i.e stamp duty, legal fees, and others), there is a discomfort in knowing the level of debt that first home buyers and single parents will need to service for years to come.

Once again policy, or more correctly the right policy, really matters.

It seems that the current Government schemes are a catch-22, swapping early and/or easier access to home ownership with a debt level that the target demographic may not be ready to take on. The new price caps open up a higher probability for certain price bands to inflate, lifting prices on what was once thought of as “affordable”. This potentially prices out the next generation of first home buyers and single parents, creating a multiplier effect of reliance on Government incentives.

One could argue that the number of properties available under this scheme is minute compared to the number of transactions that happens in the open market. Whilst this is true, the argument for establishing these schemes is the hurdle of saving for a deposit. Increasing property prices as a result of the scheme will re-invent the wheel of issues.

The current increase in property prices are due to an imbalance in demand and supply of housing stock. These Government schemes add to the demand, and thus must be balanced with schemes that will at least create the same amount of supply. At present our property market is sheltered from international demand, thus now is potentially the most affordable and advantageous time for first home buyers and single parents to enter the market; providing they are comfortable with the level of debt.