What is the future for Investors?

From the Desk of the Chief Economist

The rental housing crisis is widely reported across Australia, with the evidence mounting: rental prices climbing to extreme heights, renters unable to secure tenancy, and property managers flooded with multiple applications for the one property.

So why are rental yields falling in many capital cities? And what does this mean for investors?

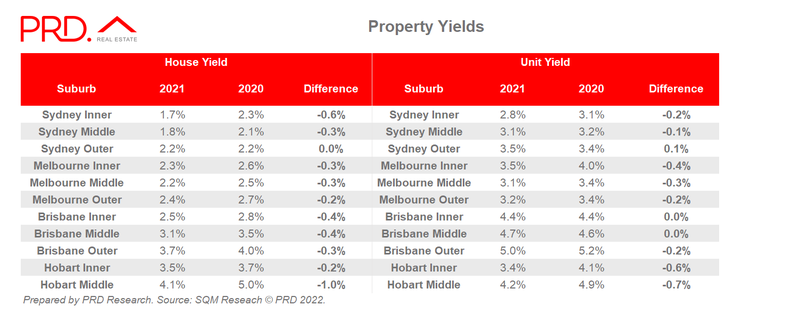

Falling Rental Yields

Gross rental yield calculates the amount of rental income you can receive over a year. It is measured against the market value (or purchase price) of the property.

Net rental yield takes into account all other costs (body corporate, insurance, repair costs, etc) specific to the property. Net rental yield is a more accurate measure, however, it is limited to the specificities of each property and investor. Thus, gross rental yield is more widely quoted in research and the media.

In the 12 months leading to 31 December 2021, gross house rental yield has fallen in most of Sydney, Melbourne, Brisbane, and Hobart; except for Sydney outer ring (10-20km from Sydney CBD). Gross unit rental yield follows the same pattern - with only Brisbane inner ring (0-5km from Brisbane CBD), Brisbane outer ring, and Sydney outer ring displaying stable and/or increasing rental yield.

Asset Value vs Rental Value

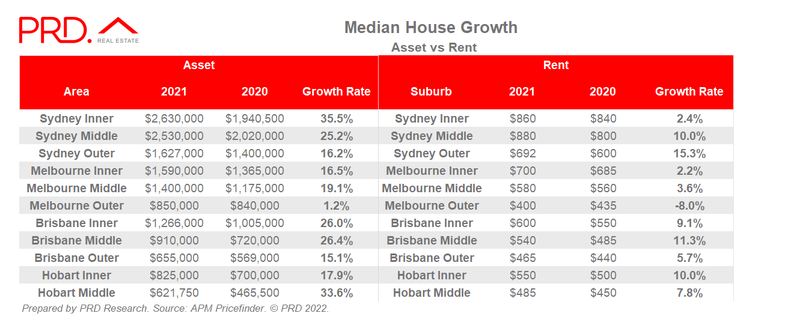

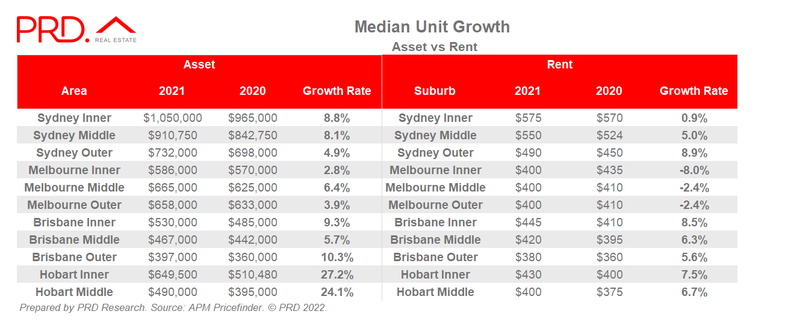

Why are rental yields falling? The answer is simple. Within the same time frame, median sale price growth (i.e asset value) have outpaced median rental price growth (rental value).

For example, the annual median house sale price growth in the Sydney inner ring (0-5km from Sydney CBD) was 35.5%. However, the median house rental price growth was 2.4%. Similarly, annual median house sale price growth in the Hobart middle ring was 33.6%, much higher than the median house rental price growth of 7.8%.

Because rental yield is calculated based on rental income received measured against property value, this causes rental yields to fall. How far rental yields fall (or increase), depends on the balance between median sale price growth and median rental price growth within the same period. For example, in the Sydney outer ring, median house sale price grew by 16.2%, whereas median house rental price grew by 15.3%. Thus rental yield has remained stable at 2.2% between 2020 and 2021, as growth in rental value is similar to the asset value.

Dissecting the Market

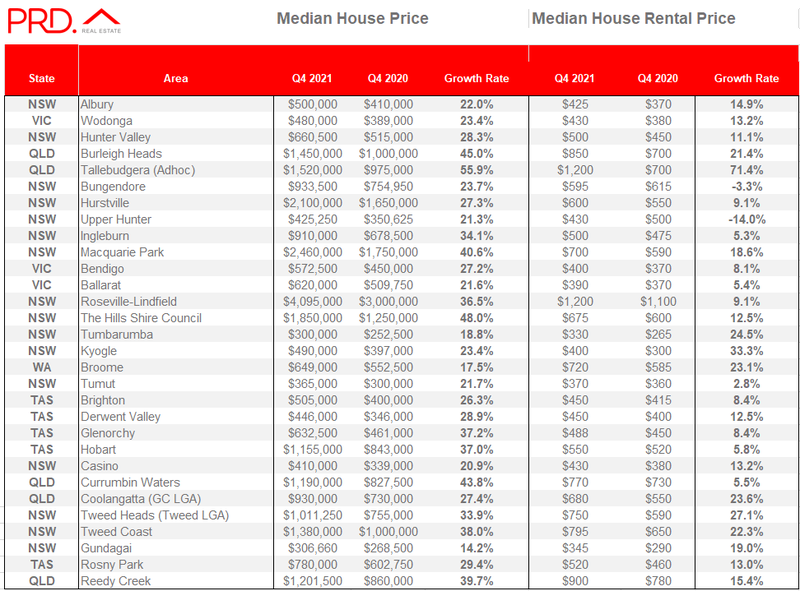

Looking at a random selection of different markets across Australia, there is a majority trend of declining rental yields. Though, there remain some exceptions, for example in Tumbarumba (NSW), Kyogle (NSW), Gundagai (NSW), and Broome (WA), to name a few.

In the areas where rental yields have fallen, for example in Albury (NSW), Bendigo (VIC), Glenorchy (TAS), Burleigh Heads (QLD); there is an imbalance between stock for sale (supply) and the number of buyers (demand). Many areas are undersupplied, causing the median house sale price to increase exponentially.

It is important to remember, each market within Australia is unique, even if there are similar trends. This is due to local supply and demand balance, local economic structure, demographic make-up, and future developments planned for the area. Because of this, an investor needs to dissect each market to get a holistic set of information prior to making a decision.

For example, based on the tables of data above, is it more profitable to invest in Brisbane Inner ring or Middle ring? Brisbane Middle ring provided a more affordable asset entry point, but Brisbane Inner fetched a higher rent value. Based on rental yield movements the answer is neither, as, within the same time frame, both areas experienced the same level of rental yield decline. It thus depends on the investor’s financial situation, availability of preferred stock, and the target market.

Moving Forward – What does this mean for Investors?

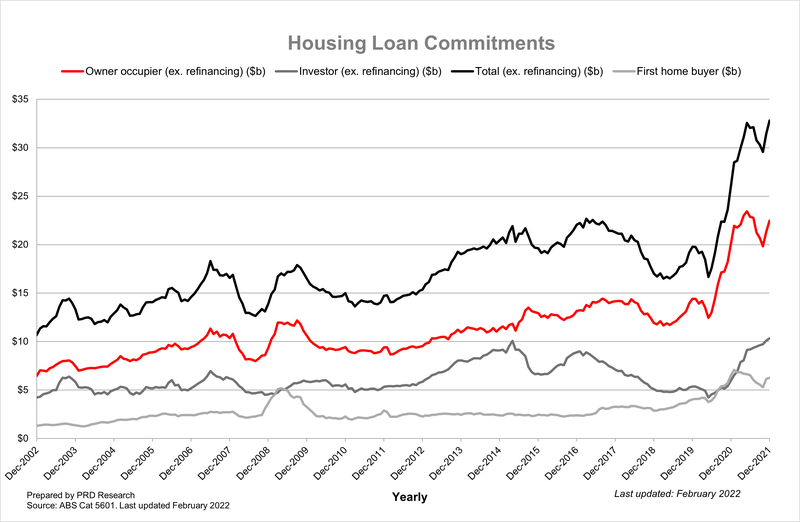

Investors have made a comeback since COVID-19, committing to $10.3B in investor loans as of December 2021. This is a 73.9% growth in the past 12 months ($5.9B in December 2020). The proportion of investor finance also grew during this time, from 23% of total housing loan commitments in December 2020 to 32% in December 2021.

Investors rely mostly on two key indicators in their decision making before purchase: rental yield and vacancy rates. Investors, in general, choose areas with a high and/or increasing rental yield and low or declining vacancy rates. Together this makes an ideal investment environment, as the investor benefits from high(er) rental returns and quick(er) occupancy for better income cash-flow.

A falling rental yield is not necessarily doom and gloom for an investor, especially if:

- a) Median rental price growth is high, for example, 15.3% for houses in the Sydney outer ring and 11.3% for houses in the Brisbane middle ring

- b) Vacancy rate is low and/or on a declining trajectory towards 0.0%, as it means quicker occupancy and a steadier level of income cashflow

- c) Average days on the market (to rent) is on a declining trend

- d) Planned future project developments focus on infrastructure and commercial development, which will improve liveability for residents and increase economic activity. This has the potential of drawing more people to the area, and if there is not enough stock for sale then the only choice is to rent.

The two-fold major source of uncertainty for investors in the immediate future is the Federal budget 2022 (due to be handed down in late March) and the Federal election 2022 (due to be held sometime in May). These two events may change the course for investors, as there might be policy changes that impact taxation, deduction, and purchasing capabilities. Any potential changes in negative gearing will create uncertainty and lower investor confidence.

That said, the available stock is low throughout Australia, both in capital cities and regional areas. With the relaxation of interstate migration and the opening of international borders, coupled with a lagging construction industry; the imbalance between supply and demand is imminent. This rings true in both the sales and rental market, and this fundamental issue will not be solved by either March or May.