Will a cash rate hike result in higher property prices?

From the Desk of the Chief Economist

Speculation of whether the Reserve Bank of Australia (RBA) will increase the cash rate has been rife since the very first-time inflation hit outside the healthy 2-3% band in June 2021. This has caused a stir in property market, whether we will see a cooling in property prices.

The RBA continues to maintain 0.1% cash rate for the past 3 months in 2022, citing the need to see a sustainable level of both inflation rates and wage growth before a cash rate hike. This answer has kept us on our toes and continue to build uncertainty in the market.

However, as inflation continues to increase and evidence of higher wage growth emerge, there is now, more than ever, speculation that the RBA will increase the cash rate in June.

The question is, will property prices increase? Do we need to worry?

Historical Evidence

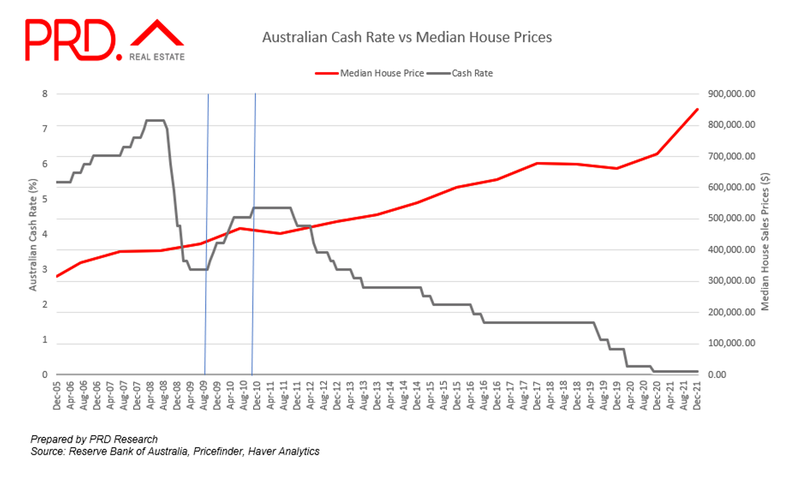

The RBA increased the cash rate multiple times between October 2009 – November 2010. The RBA increased the cash rate by 25 basis points in October 2009, and again November 2009, December 2009, March 2010, April 2020, May 2010, and November 2010.

The cash rate went from 3.25% to 4.75% in the space of 12 months, amounting to an increase of 175 basis points in the space of just a little over 12 months.

Historically speaking, if we look at the graph, the first cash rate cut in October 2009 did not immediately result in property prices cooling. In fact, property prices went up, due to the potential of another cash rate increase in the next months. Buyers wanted to be able to purchase their property at the new October 2009 cash rate before there were more.

History tells us it took several cash rate hikes, in succession, over a period of roughly 12 months, before we saw a cooling down in price. This suggests that there is a time-lag between a cash rate hike event and the translation into property prices.

What can we expect from a cash rate increase?

Technically speaking, a higher cash rate, and if adopted by banks means higher interest rates for mortgage loans. This will limit or decrease the amount of people can borrow – thus less demand. It can also mean those who are unable to meet mortgage home loan repayments may be forced to sell – thus more supply

This impacts supply and demand balance, and depending to what extent is this balance moved, prices will also move.

History tells us that buyers react in the opposite manner when there is a cash rate hike, entering the market in fear of another (cash rate hike) and before their borrowing power lessen considerably. History also tells us there is a time lag between when cash rate movements and property prices.

Furthermore, our current property market situation differs greatly than 2009/2010.

The current demand we have is more so local demand, due to a triage of factors: COVID restrictions, Federal Government home-ownership grants, and demographic changes. We are yet to receive the normal pre-pandemic level of international demand for property. We are yet to have the pre-pandemic local and international “normal” type of demand.

What’s more, we still have a significant supply issue, with less new ready-to-sell stock coming into the market due to rising construction costs.

The deep supply and demand imbalance right now may result in an even longer lag time between when cash rate hike will translate into property prices.

Moving forward – should we worry?

Should we worry about the cash rate hike, and how it will impact the property market?

Or is the more prevalent question: what will the banks, and in particular your bank, will do?

There is no law (in Australia) that states each bank or lender must follow the RBA’s cash rate patterns. Experience has shown banks fully passing on a change in cash rate or in a certain manner, depending on the needs of the bank.

Already we have seen many non-bank lenders discontinue the 1.99% historical low fixed interest rate since mid/late last year 2021, and some banks increasing their variable rates in the past couple of months in early 2022. This is even whilst the RBA has remained its 0.1% cash rate stance.

Thus, in a sense, people are already dealing with a change in the mortgage lending space, and potentially in their mortgage home loan repayments as well.

We have also seen APRA tighten lending practices in November 2021, for banks to assess borrowers at a higher rate. Therefore, there is extra buffer built in, which could potentially translate to borrowers are already safe guarded against cash rate hikes.

It will most likely be borrowers that are on variable rates that feel the impact of the cash rate hike. As of December 2021, the family income to meet mortgage repayments were at 37%; and most measures will classify 30% or more as heading towards mortgage stress

Whether or not the RBA will increase their cash rate in June 2022 cannot be predicted 100%. However, the RBA has changed their stance in the past couple months, from no cash rate changes until 2023 to potentially a cash rate change when the situation is deemed fit.

How the property market will react when a cash rate change occurs cannot also be 100% predicted, due to the multitude of other factors at the time of the change – in particular the level of (or rather, imbalance of) demand and supply. Furthermore, the Australian property market is not uniform, there are markets within markets – both location wise and stock type wise. Again, the demand and supply dynamics within each market will determine to what extent a cash rate change will impact the market.