RBA and Federal Budget 2021 Update: Improving Affordability and Accessibility to the Housing Market

From the Desk of the Chief Economist

May has proven to be an extremely important month for the Australian economy, with the release of the Reserve Bank of Australia’s statement on monetary policy, days prior to the release of the 2021 Federal Budget.

Both parties agreed that although there is no playbook to speak to in a COVID-19 pandemic situation, the Australian economy proved to be resilient. Despite the enormous contraction from April 2020 onwards there has been rapid recovery led by a shift in demand from services to goods. Viewed as one of the few countries able to contain the virus, Australia is also part of a very small group of countries that has economically bounced back from COVID-19.

The economics of the housing market is dependent upon the balance of demand and supply, both of which are heavily influenced by monetary policy (enacted by the Reserve Bank of Australia – RBA) on cash rate matters and fiscal policy (enacted by the Government, at all three levels) on grants, schemes, and taxation matters.

Fiscal Policy – the Federal Budget

The Federal Budget 2021 had one theme and mantra: “Keep the recovery going”.

In doing so there were surprise tax cuts, a strong infrastructure program, the pre-released housing measures, extended investment incentives, and government spending at a healthy 27% of GDP; all designed to ensure Australia’s economic recovery momentum.

There are direct and indirect fiscal policies that will impact the housing market. Direct policies are categorised as those targeting accessibility into homeownership. Indirect policies are those that impact the household income, and can influence one’s decision in regards to housing matters – their ability to purchase, rent, and invest.

Direct policies

Federal Budget 2021 is also dubbed the “Housing Budget” by many, due to its specific and high number of policies addressed towards the housing market.

- Family Home Guarantee. 10,000 guarantees made available over 4 years to single parents with dependents, allowing them to purchase homes with a 2% deposit

- New Home Guarantee. This will provide additional 10,000 places in 2021-22. First home buyers seeking to build a new home or purchase a newly built home can do so with a 5% deposit.

- First Home Super Saver Scheme. From 1st July 2022, the maximum voluntary superannuation contributions that can be released will increase from $30,000 to $50,000. Voluntary contributions from 1st July 2017 up to the current limit of $15,000 will count towards the total amount to be released.

- $774.8M over 2021-22 for existing applicants to extend construction commencements from 6-18 months in the HomeBuilder program.

- $124.7M over 2021-22 to States and Territories under the National Housing and Homelessness Agreement, to add to public housing stock or to meet wages requirements on social and community services wages.

- The minimum age for the downsizer contribution has been reduced from 65 to 60, and eligible Australians can make a one-off post-tax contribution of up to $300,000 per person (or $600,000 per couple).

- $10.0B reinsurance pool. This underwrites guarantee on the reinsurance pool is anticipated to reduce insurance premiums by approximately $1.5B for 500,000 policyholders and will make properties more saleable.

Other than no changes to negative gearing, it seems that the mum and dad investors are not the direct focus of Federal Budget 2021.

Indirect policies

Indirect policies can take many forms, with two overarching goals: a) increase disposable income for individuals and businesses, b) stimulate the economy as a whole through infrastructure projects that lead to job creation and increase production.

- Extension of stimulus payments to low and middle-income earners by retaining the Low and Middle-Income Tax Offset (LMITO) for the 2021-22 financial year.

- Eligible individuals will receive a reduction in tax of up to $1,080.

- Reduced tax rate of 25% for small and medium companies from 1st July 2021. Alongside this, businesses will be able to apply temporary full expensing and temporary loss carry-back. These two measures have been extended to allow businesses increased cash flow.

- $15.2B committed to infrastructure developments, spread across multiple projects across capital cities and regional areas in all States and Territories.

- Boosting Apprenticeships Program, which can provide a wage subsidy of up to $7,000 per quarter. Self-Education Expense Deductions will also be completely deductible, with the initial $250 removed.

Monetary Policy – the RBA

In its statement on monetary policy for May 2021, the RBA noted the resilience of the household disposable income. Throughout COVID-19 it extraordinarily did not decline, infact it picked up. Households were saving more during COVID-19, as there was a spike in income due to stimuluses introduced by fiscal policy, however households did not spend as they normally did. There is a substitution in consumption, with some choosing to spend in the property market as opposed to other big-ticket items (such as overseas holidays) or investing in the share market (which proved to be more volatile).

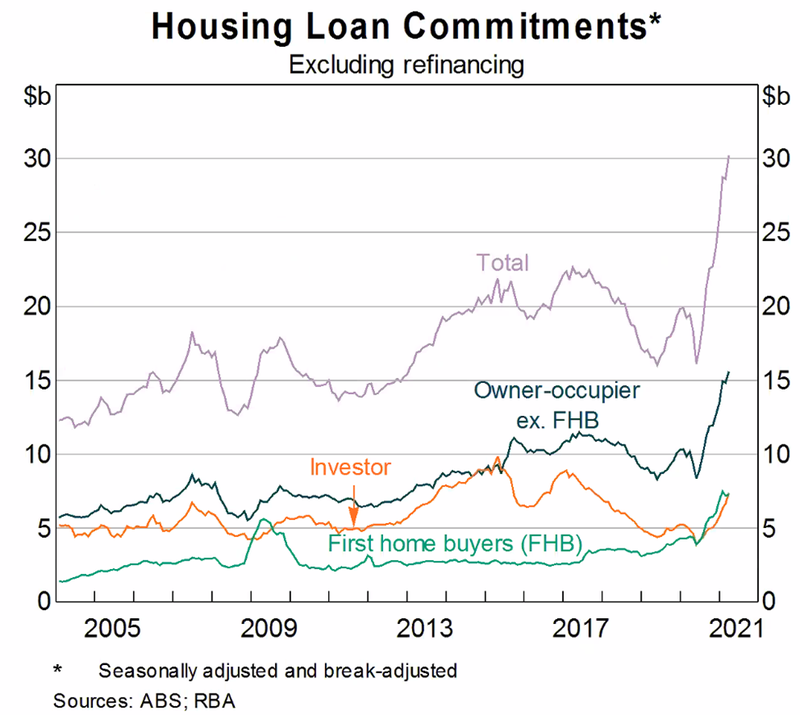

Housing loan commitments have soared in 2021 due to a combination of factors: household income resilience and a change in spending habits, fiscal policies such as HomeBuilder and the expansion of the First Home Loan Deposit Scheme, and extremely low home loan mortgage interest rates.

Owner-occupiers (excluding first home buyers) lead housing loan commitments, and there is a clear spike in first home buyer activity. Investors are making a comeback in early 2021, with a sharp incline in their recent housing loan commitments. The RBA made a note that there is a dampening effect in housing loans, as although there are new loans being established there are also many who are paying off mortgages and/or building their offset account(s).

The RBA maintains its position on cash rate movements, committing to keeping the cash rate at a historical low level of 0.1% until such a time in which: a) inflation is back within the 2-3% band and b) wage growth is closer to target level of beyond 3%.

Moving forward

Policy, or more correctly the right policy, really matters.

The RBA has decided to not increase the cash rate until earliest 2024, due to price and wage growth growing at a lower speed than hoped. Although a decline in the home loan affordability index and an increase in the percentage of income as a proportion of house mortgage loans are acknowledged, the RBA maintains the position that applicants are still being assessed on a higher rate for borrowing and that many are borrowing within their limit.

Accessibility to home ownership, to those who are able to service the mortgage but are challenged in establishing a 20% deposit, is suggested as a solution.

Here fiscal policy plays a strong hand, with the Federal Budget 2021 introducing measures that allow more of certain demographics (first home buyers and single parents) to access the property market. The Federal Government has dipped its toe in increasing housing stock supply, by: a) reducing the age threshold for downsizers, b) underwriting guarantees in the insurance pool, and c) extending the construction commencement of HomeBuilder.

We can foresee that this will increase housing loan commitments, regardless of the buyer type. In the current housing market that many will describe as “on fire”, there is a catch-22 situation. Those who previously could not access home ownership now have a better chance, and this will absorb properties at the lower end of the market. However supply is yet to catch up, and with increasing demand lays the danger of increasing house prices, ultimately resulting in higher loans and debt to income ratios.

At present, there are still many uncertainties, as both the RBA and the Government are observing a society that are behaving in ways that they have not seen. This is due to varying levels of income and what world lays before us as we continue our journey with COVID-19.

The next six months will be extremely interesting to see how both monetary and fiscal policies play together in ensuring affordability and accessibility within the housing market.