Sydney - Affordable & Liveable Property Guide 2nd Half 2018

Between 2017 and 2018, Sydney Metro median house prices have softened by -5.6%, whilst units have softened by -2.5%. Affordable options can be found in Sydney’s South Western suburbs.

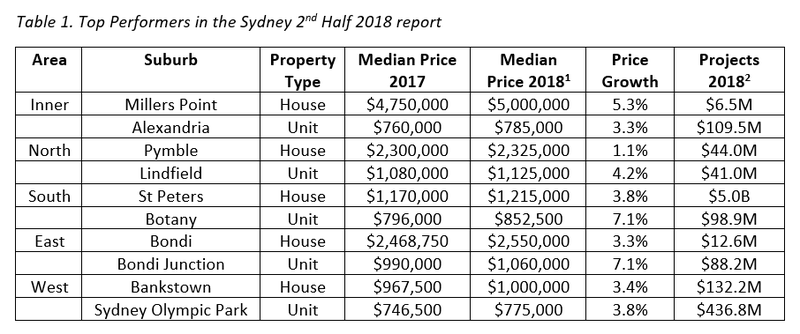

Affordable Suburbs - Sydney

Between 2017 and 2018, Sydney Metro median house prices have softened by -5.6%, whilst units have softened by -2.5%. Affordable options can be found in Sydney’s South Western suburbs.

A key finding in the Sydney

Affordable and Liveable Property Guide 2nd Half 2018 is that all

affordable and liveable suburbs identified have declining annual median house

or unit price growth. Thus, instead of showcasing suburbs with the highest

price growth, which has been the trend over the past 4-5years, for the first

time, it became an exercise in minimising the decline in capital growth. That

said, this is great news for first home buyers, as this means more suburbs

within 20kms are becoming affordable.

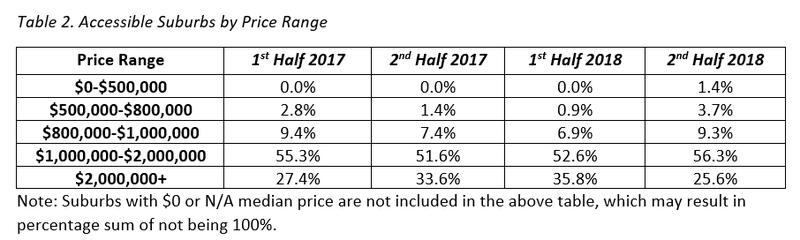

The number of first home buyers in New South Wales increased by 68.8% over the past 12 months to the June 2018 quarter, which is only a slight decline from the 74.9% growth over the past 12 months to December 2017 quarter3. This confirms that there is a continuing return towards a sustainable market. Table 2 provides the percentage of suburbs that is available for house buyers.  Liveable Suburbs

- Sydney

Liveable Suburbs

- Sydney

In the 12 months, between the 2nd half of 2017 and the 2nd half of 2018, there has been some important shifts in price brackets for houses in Sydney. For the first time in 5 years, the lowest bracket of houses below $500,000 have emerged. These have been very low in activity, with only a handful of sales recorded in these instances. Across the entire price range, affordability has increased as the Sydney market has softened to a more sustainable level. Access to suburbs priced between $500,000 to $800,000 have more than doubled to 3.7%. Access to the $800,000 to $1,000,00 bracket have also increased, as did the still dominant $1,000,000 to $2,000,000 price bracket. All these gains have shifted from the upper price range of $2,000,000+, which reduced by -8.0% in the past 12 months, down to 25.6%. This cooling is positive news for all future property buyers, with a return to sustainable pricing expected to help better manage growth levels in the future.

Highly affordable suburbs, those with a maximum house price of the average state loan plus a 135% deposit exist. 74 suburbs are within this price bracket, significantly more than the 8 identified in the 1st half report. This reinforces that the market is moving into a more affordable position for buyers.

Despite this, many of the Sydney suburbs fail to meet the liveability criteria set. 160% (houses) and 60% (units) premiums needed to be added to the New South Wales average state loan, which is extremely close to the 163% (houses) and 58% (unitss) premiums that needed to be added to purchase Sydney Metro median price. This suggests that those looking for basic liveability aspects must be willing to pay extreme premiums, making the cost of liveability quite high in Sydney.

Despite being identified as affordable and liveable suburbs in the 1st half of 2018, Milperra (houses), Dee Why (units) and North Rocks (units) all failed to meet the liveability criteria in the 2nd half of 2018, making them ineligible as affordable and liveable suburbs this half. There is a need for strategic action to improve liveability in Sydney.

Considering all methodology criteria (property

trends, investment potential, affordability, project development, and

liveability factors), Table 2 and 3 identify key suburbs that property watchers

should look out for.

Affordable & Liveable Suburbs - Sydney

Sydney’s rental market has experienced a softening in

quarterly price growth since Q1 2018, decreasing by -3.8% to $500 for 3-bedroom

houses and by -1.8% to $550 for 2-bedroom units. That said, over the past 12

months to Q2 2018 median weekly rents increased by 3.1% for 3-bedroom houses

and remained stable for 2-bedroom units. The rising vacancy rate of 2.7% as of

June 2018, and the increasing supply of unit stock, is placing downward

pressure on the rental market. Investors are urged to hold onto their assets,

lock in prices, and secure longer tenancies. Future investors are urged to buy

into more affordable suburbs to minimise risks.

Sydney’s rental market has experienced a softening in

quarterly price growth since Q1 2018, decreasing by -3.8% to $500 for 3-bedroom

houses and by -1.8% to $550 for 2-bedroom units. That said, over the past 12

months to Q2 2018 median weekly rents increased by 3.1% for 3-bedroom houses

and remained stable for 2-bedroom units. The rising vacancy rate of 2.7% as of

June 2018, and the increasing supply of unit stock, is placing downward

pressure on the rental market. Investors are urged to hold onto their assets,

lock in prices, and secure longer tenancies. Future investors are urged to buy

into more affordable suburbs to minimise risks.

In the 2nd half of 2018, Sydney will see approximately $15.3B in future project developments commence. The focus is on infrastructure, which is critical to attract population growth and commercial activity for continued economic productivity. Major projects during this period are the $5.0B Westconnex M4-M5 link, the $1.0B Parramatta Light Rail network, and the $955.0M Sydney Central Station and Central Walk works. This presents many opportunities for astute investors to capitalise on untapped property price growth potential in nearby suburbs.

Methodology

This PRD Affordable and Liveable Property Guide 2nd Half 2018 analyses all suburbs within the Greater Sydney area in a 20km radius from the CBD. In doing so the below factors and methodology were considered:

- Property trends – all suburbs considered will have a minimum

of 20 transactions for statistical reliability purposes, with positive price

growth from 2017 to 2018.

- Investment – as of June 2018 the suburb will have an

on-par or higher rental yield than Sydney Metro, and an on-par or lower vacancy

rate.

- Affordability – suburbs with a median price below the maximum

sale price of state average home loan plus allocated premium percentage. In

this report 160% (houses) and 60% (units) was added to the average New South

Wales home loan, which was $484,829 as at June 2018. This is below the 163%

(houses) and 58% (units) premiums needed to purchase the Sydney Metro median

price, thus more affordable for buyers.

- Project development – the suburb has a high total estimated

value of project development for the 2nd half of 2018. This ensures

sustainable economic growth, having a positive effect on the property market.

- Liveability factors – this includes ensuring low crime rate, availability of amenities within a 5km radius (i.e. schools, green space, public transport, shopping centers, and health care facilities), and an unemployment rate on par or lower in comparison to the state average (as determined by the Department of Jobs and Small Business, June Quarter 2018 release).

Affordable and Liveable Property Guide 2nd Half 2018 - Sydney